(General Studies III – Environment section – Conservation, Environmental Pollution and Degradation, Environmental Impact Assessment.)

- The European Union’s Carbon Border Adjustment Mechanism (CBAM), a measure designed to impose carbon costs on imported goods, is being criticised by India and other developing nations as discriminatory.

- With the definite phase set to begin in 2026, the CBAM poses a serious challenge to India’s exports, particularly in sectors such as iron, steel, and aluminium, which constitute a significant portion of India’s trade with the EU.

| CBAM: A Discriminatory Measure Shifting the Responsibility: Experts argue that CBAM disproportionately burdens exporters from developing nations by holding them accountable for emissions embedded in their exports. This contravenes the principle of Common but Differentiated Responsibilities and Respective Capabilities (CBDR-RC) under the UNFCCC, which acknowledges the differing capacities of countries to address climate change.Exacerbating Inequities: Noted economists emphasize that CBAM ignores historical emissions by developed nations, instead penalizing countries with emerging economies for their developmental emissions. This approach deepens the divide between the Global North and South, fostering inequality in global climate governance.Revenue Retention: CBAM retains revenues within the EU, depriving developing nations of financial support for technology transfer and capacity-building, which are essential for adopting sustainable practices. Critics call this a unilateral move that disregards the cooperative nature required for addressing climate issues.Limited Adaptation Time: Experts highlight that developing countries have not been afforded the decades-long timelines enjoyed by the EU to adapt to stringent climate measures, making CBAM particularly onerous. |

Proposed Arguments and Solutions for India –

- Demand for Adequate Preparation Time: Highlight the disparity in timelines for emission reduction targets.

- While the EU began its climate action in 1990, developing countries, including India, lack similar historical timelines to adapt to mechanisms like CBAM.

- Call for Revenue Sharing: Advocate for sharing CBAM revenues to fund capacity-building, technology transfer, and sustainable development in developing economies.

- Promote Equity-Based Accounting (EBA): Push for a fairer system of emission accountability based on principles of intra-generational equity and inter-generational equity.

- Introduce a tariff calculation formula incorporating factors like per capita GDP, per capita emissions, and historical contributions to climate change.

- Strengthen Retaliatory Mechanisms: Collaborate with other developing nations to develop counter-measures that reflect their economic and developmental heterogeneities.

- Propose a collective response at global platforms like COP29.

- Leverage Multilateral Platforms: Use platforms such as the United Nations Framework Convention on Climate Change (UNFCCC) to contest CBAM’s lack of compensatory and distributive justice.

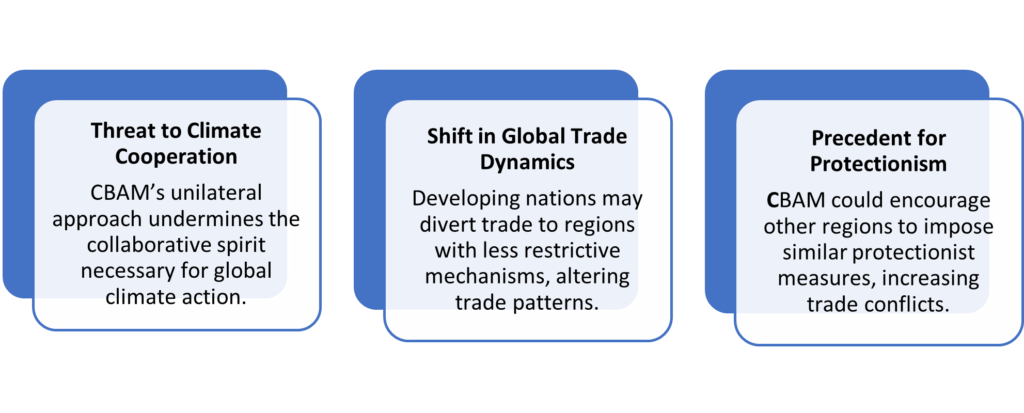

| Broader Implications for Global Trade |

| To effectively counter CBAM, India must adopt a multi-pronged strategy emphasizing fairness, equity, and international collaboration. Advocating for adequate preparation time, revenue sharing, and equity-based accounting principles will not only strengthen India’s position but also uphold the principles of CBDR-RC. |